NOI Wins: The Real Places AI Delivers in Commercial Real Estate

June 05, 2026 / Bryan Reynolds

Custom Software for Commercial Real Estate: Where AI Actually Pays Back in 2026

The era of zero-interest-rate technology experimentation in commercial real estate is officially dead. In 2026, the industry exists in a state of profound macroeconomic recalibration, characterized by elevated capital costs, massive debt maturities, and a ruthless flight to quality among commercial tenants. Against this unforgiving backdrop, the discourse surrounding artificial intelligence and custom commercial real estate software has fundamentally shifted. The market no longer rewards speculative pilot programs; it demands immediate, quantifiable returns on investment that drop directly to the net operating income line.

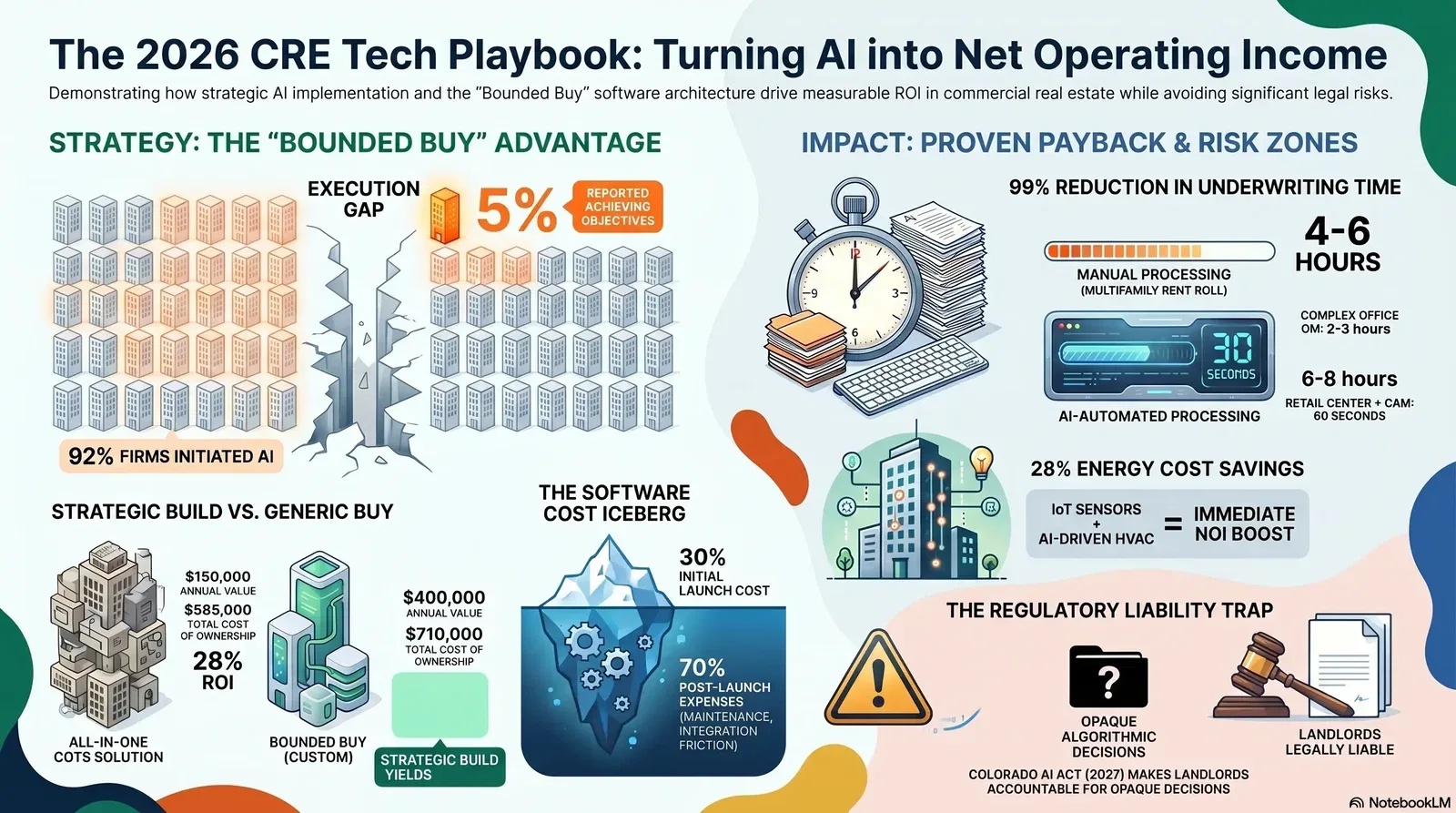

The enthusiasm for technological transformation remains unprecedented, yet the execution gap is staggering. Industry data reveals that 92 percent of corporate occupiers have initiated artificial intelligence programs, a massive surge from just 5 percent a mere three years prior. However, an alarming reality underpins this adoption metric: only 5 percent of these organizations report achieving their primary technological and financial objectives. Broader surveys of infrastructure and operations leaders further contextualize this failure rate, indicating that only 28 percent of artificial intelligence use cases fully succeed and meet their expected return on investment, while a full 20 percent fail outright.

This catastrophic failure rate is not a reflection of the technology's potential, but rather a profound misunderstanding of where and how software creates leverage in a real estate portfolio. Buying a generic artificial intelligence subscription does not salvage an obsolete Class B office building, nor does forcing a proprietary, off-the-shelf property management system to handle bespoke joint venture distributions create a competitive advantage. Custom software and artificial intelligence pay back in highly specific, highly process-intensive domains: the leasing pipeline, complex property valuation, and physical asset operations. Conversely, these technologies destroy value—and introduce severe regulatory and legal liabilities—when deployed without rigorous data security, architectural discipline, or compliance frameworks.

Adopting the "They Ask, You Answer" methodology, this comprehensive analysis breaks down the exact financial mathematics of commercial real estate technology in 2026. It explores the total cost of ownership for custom versus commercial software, details the precise workflows where artificial intelligence generates massive labor savings, and issues a stark warning regarding the new wave of algorithmic legislation sweeping the sector.

The Macroeconomic Forcing Function of 2026

To understand the urgent mandate for technological efficiency, one must first examine the macroeconomic forces constraining commercial real estate operators. The market is defined by expensive capital, stringent lending standards, and highly variable asset performance. Real estate organizations can no longer rely on cap rate compression or cheap debt to generate outsized returns. Value must now be manufactured purely through operational efficiency, precise market timing, and rigorous, systemic cost control.

The Office Sector: A Tale of Three Markets

The U.S. office sector exemplifies the current market bifurcation, forcing operators to deploy technology just to remain solvent. The national office vacancy rate was projected to reach a cyclical peak of 21.6 percent in the second half of 2025, leaving vast swathes of secondary and tertiary inventory struggling for relevance. However, this aggregate figure masks a highly fragmented reality. The sector has effectively split into three distinct tiers of performance, requiring entirely different technological strategies.

At the top of the market, demand for modern, amenity-rich spaces remains remarkably resilient. Approximately 30 percent of Class A office buildings are fully occupied, and another 20 percent maintain vacancy rates below 15 percent. In the first quarter of 2026, the office market recorded 3.5 million square feet of quarterly occupancy gains, marking the third consecutive quarter of positive net absorption. Major metropolitan hubs drove this recovery, with San Francisco contributing 1.6 million square feet and New York adding 1.5 million square feet of net absorption.

Furthermore, the premium tier of the market is achieving record pricing power. The first quarter of 2026 saw over 4 million square feet of leasing volume executed at starting rents exceeding $100 per square foot (Full Service Gross), the highest first-quarter volume ever recorded for such high-rent transactions. Same-asset rents increased by 0.8 percent over the past year, led by aggressive growth in markets like Miami (+4.0 percent), Orlando (+3.0 percent), and New York (+2.2 percent).

Conversely, the broader market remains under severe distress. Office delinquency rates have continued their upward trajectory, growing by 74 basis points between December and March to reach 11.41 percent. Total office inventory declined by 9 million square feet in the first quarter, marking a massive contraction of more than 25 million square feet from the peak in late 2023. Construction has ground to a near halt, with less than 1 million square feet breaking ground in the first quarter, leaving the active pipeline at 22.3 million square feet—the lowest volume ever recorded in modern tracking. For operators holding distressed assets, the integration of custom underwriting software to rapidly evaluate conversion feasibilities (such as office-to-residential or office-to-life-science) is no longer a luxury; it is a matter of survival.

The Industrial Sector: Stabilization and the Power Mandate

The industrial and logistics sector presents a starkly different profile, though one equally reliant on advanced technological integration. Following a period of hyper-growth, the market has stabilized on a highly solid footing. In the first quarter of 2026, the national industrial vacancy rate declined slightly from its late-2025 peak to 7.0 percent. Net absorption demonstrated exceptional strength, reaching 40 million square feet for the quarter—a 52 percent year-over-year increase and the strongest start to a year since 2023.

Industrial demand is overwhelmingly skewed toward modern facilities. Occupiers are aggressively upgrading their spaces to accommodate advanced robotics, artificial intelligence systems, and the significantly higher power capacities required for modern logistics. Properties delivered since 2020 accounted for 68 million square feet of the trailing absorption, with nearly half of that activity occurring in mega-facilities larger than 500,000 square feet. Meanwhile, new supply has eased considerably, with quarterly completions falling 27 percent year-over-year to 54 million square feet, the lowest level since mid-2017.

In this sector, the technological mandate is operational. Industrial landlords are required to deploy highly sophisticated Internet of Things (IoT) sensors and predictive maintenance algorithms to manage the immense energy loads and HVAC requirements of these automation-ready facilities.

| Asset Class | Key Market Indicator (Q1 2026) | Strategic Technological Implication |

|---|---|---|

| Premium Office | >$100/sf starting rents, 3.5M sf net absorption | Deploy advanced CRM and tenant experience apps to retain high-paying occupiers. |

| Distressed Office | 11.41% delinquency rate, 21.6% peak vacancy | Utilize custom AI underwriting to rapidly model complex asset conversions and repositioning. |

| Industrial | 40M sf net absorption, vacancy stable at 7.0% | Implement IoT predictive maintenance to handle high-power, automation-ready logistics hubs. |

| Multifamily | Shrinking operating margins, rising tenant expectations | Mandate centralized leasing platforms to reduce onsite administrative headcount by up to 35%. |

Data synthesized from JLL and Cushman & Wakefield Q1 2026 MarketBeat reports.

The Build vs. Buy Dilemma: Mastering the Total Cost of Ownership

The decision to modernize operations invariably forces real estate executives into the classic software procurement dilemma: should a firm build a custom solution or buy a commercial off-the-shelf (COTS) platform? The property technology (PropTech) sector is undergoing massive consolidation, with over 200 mergers and acquisitions occurring in 2024 alone, a pace expected to double by the end of 2026 as traditional real estate companies buy up innovation. Yet, for the firms deploying the software, the financial reality is far more complex than initial vendor demonstrations suggest.

The Software Cost Iceberg

When analyzing commercial property management systems, the initial sticker price is deeply misleading. Hidden costs frequently inflate the total cost of ownership (TCO) for enterprise software by 30 to 50 percent within the first twelve months. The "software cost iceberg" dictates that a staggering 70 percent of a digital asset's lifecycle expenses occur post-launch, consumed by maintenance, integration friction, user training, and forced system upgrades.

Consider the financial profile of industry-standard platforms. While exact enterprise pricing is highly guarded, typical per-unit and license fees create massive capital requirements. For a mid-market portfolio of 2,000 units, base annual software fees for platforms like Yardi or RealPage might range from 50,000 to 150,000. However, implementation costs routinely add an additional 40 to 80 percent on top of the first-year subscription, pushing total year-one costs to between 80,000 and 250,000.

When real estate firms force an off-the-shelf product to perform highly specialized tasks it was not natively designed for—such as complex joint venture waterfall distributions or niche asset class conversions—they accumulate massive technical debt. Customizing rigid, proprietary platforms often results in fragile integration layers that double future maintenance efforts and drastically inflate long-term operational expenses.

| Platform Category | Typical Annual License (2,000 Units) | Implementation Surcharge | Estimated Year 1 TCO |

|---|---|---|---|

| Yardi Voyager (Enterprise) | 50,000 – 150,000 | 40% – 80% of license | 80,000 – 200,000 |

| RealPage | 60,000 – 180,000 | 50% – 90% of license | 100,000 – 250,000 |

| MRI Software | 45,000 – 140,000 | 40% – 75% of license | 75,000 – 190,000 |

Data reflects typical enterprise cloud deployments in 2026, excluding long-term maintenance and integration debt.

The "Bounded Buy" Architectural Strategy

The binary choice between building entirely from scratch and buying an inflexible, monolithic system is a false dichotomy. The architectural discipline championed by advanced consultancies like Baytech Consulting advocates for the "Bounded Buy" strategy. This approach is explicitly designed to prevent the "Vendor King" anti-pattern, where a single software vendor holds a real estate firm's entire operational data hostage.

The core principle of the Bounded Buy strategy is treating software procurement as a capability assessment, utilizing frameworks like Wardley Mapping to explicitly separate utility functions from value-creating differentiators.

Commodities and standard utility functions—such as basic general ledger accounting, standard payroll processing, or generic document storage—provide zero competitive advantage in the real estate market. These functions should be bought as commercial off-the-shelf components and integrated as quickly and cheaply as possible. Conversely, workflows that define a firm’s competitive edge—such as proprietary deal sourcing algorithms, highly specialized underwriting models, or custom artificial intelligence tenant risk assessments—deserve strategic capital investment and absolute, proprietary ownership.

By adopting an API-first, modular architecture, real estate firms can purchase specific foundational layers of a solution while building custom, proprietary applications directly on top of them. This approach prevents vendor lock-in, ensures that critical deal data remains accessible rather than trapped in proprietary file formats, and accelerates delivery timelines by utilizing modern, cloud-native components. Furthermore, leveraging AI-assisted development tools during the creation of these custom differentiators can reduce initial coding time by up to 40 percent, dramatically lowering the initial capital expenditure of a custom build.

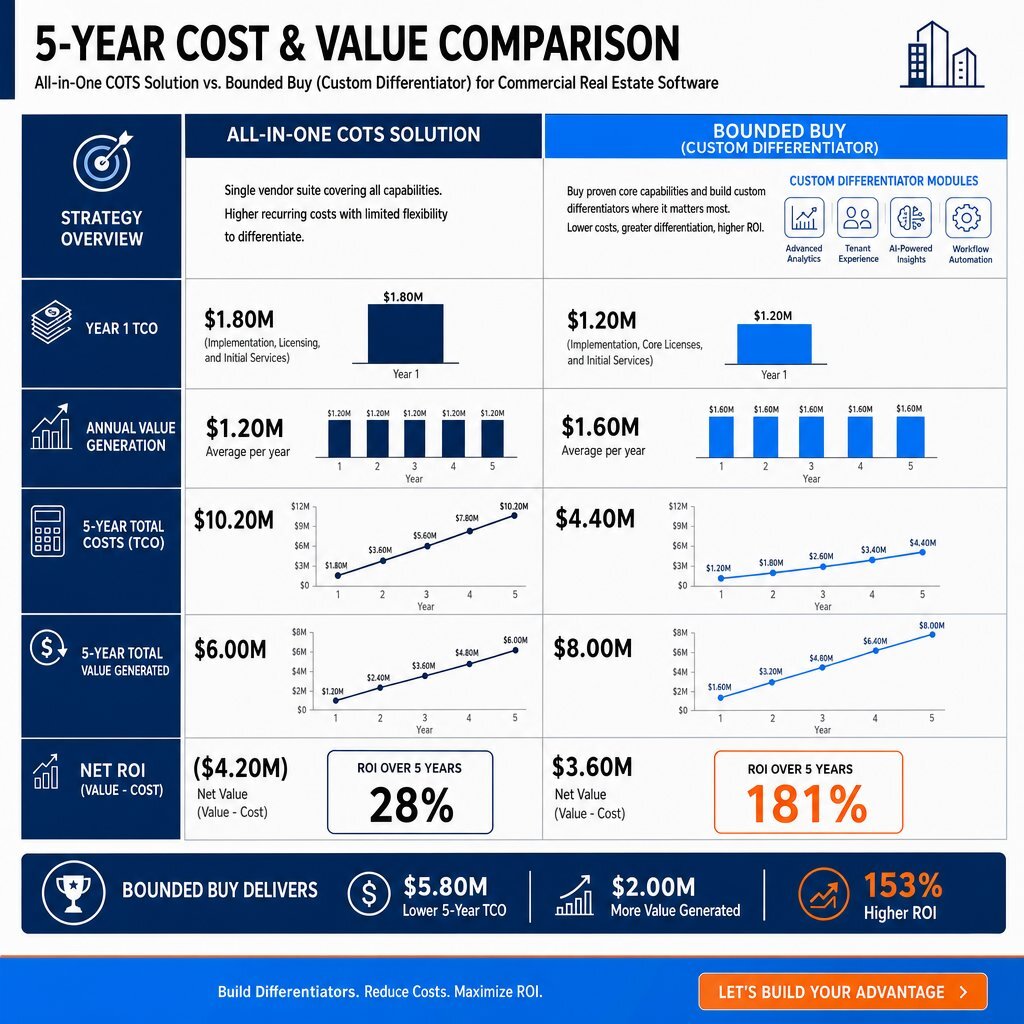

A strict financial analysis over a five-year horizon reveals the undeniable superiority of the Bounded Buy approach. While purchasing a massive, all-in-one commercial platform may present a lower initial capital expenditure, the lack of operational differentiation yields lower revenue generation. A Bounded Buy strategy requires a higher initial investment to architect and build the custom differentiator. However, because this custom module directly solves core business bottlenecks—such as executing mixed-use underwriting in minutes rather than days—it generates disproportionately higher annual value.

| Financial Metric (5-Year Horizon) | All-in-One COTS Solution | Bounded Buy (Custom Differentiator) |

|---|---|---|

| 5-Year Total Cost of Ownership | $585,000 | $710,000 (Higher initial build cost) |

| Annual Value Generation (Revenue/Savings) | $150,000 | $400,000 |

| 5-Year Total Value Generated | $750,000 | $2,000,000 |

| 5-Year Net Value (Value - TCO) | $165,000 | $1,290,000 |

| Simple ROI | 28% | 181% |

Financial modeling demonstrates that investing in strategic software differentiators yields nearly 8x the net value over a 5-year period compared to settling for generic platforms.

The Role of Fractional Financial Leadership

The integration of custom solutions and the execution of a Bounded Buy strategy fundamentally alters the financial operations of commercial real estate firms. The complexity of these transitions requires high-level strategic oversight. As real estate firms expand, they encounter intricate financial challenges that traditional accounting simply cannot solve, including complex revenue recognition models, intricate lease accounting standards, and the transition toward usage-based technology pricing models. Industry data highlights that 82 percent of real estate businesses struggle with financial complexity in the current volatile market.

For middle-market firms and growing portfolios, the cost of a full-time Chief Financial Officer is frequently prohibitive, as businesses typically do not require a full-time CFO until they reach approximately $25 million in revenue. However, navigating the procurement, deployment, and amortization of custom software requires executive-level financial modeling. Fractional CFO services bridge this critical gap, providing sophisticated financial forecasting, total cost of ownership modeling, and comprehensive ROI projection analysis without the exorbitant overhead of a full-time executive.

A highly skilled fractional CFO ensures that software investments align directly with strategic growth objectives. They mandate that clear key performance indicators (KPIs)—such as reducing invoice processing times, compressing the deal cycle, or lowering property energy consumption—are established prior to vendor selection. Without this rigorous financial oversight, artificial intelligence initiatives rapidly devolve into disconnected science projects rather than integrated drivers of net operating income. For many leadership teams, pairing this financial discipline with a clear AI ROI framework is what turns AI from a cost center into a profit engine.

The Valuation and Underwriting Engine: Eradicating Manual Data Entry

The most immediate, quantifiable, and undeniable return on investment for custom artificial intelligence software in commercial real estate occurs in the underwriting and valuation pipeline. Commercial real estate is an inherently knowledge-intensive business. Every phase of a development or acquisition project—site selection, market analysis, due diligence, and underwriting—demands deep data synthesis, pattern recognition across massive document sets, and rapid scenario modeling.

The Structural Failure of Legacy Valuation Software

For decades, the commercial real estate industry has accepted the proprietary lock-in of legacy valuation software. ARGUS Enterprise, tracing its roots to the original 1982 ARGUS DCF product, remains the institutional standard for lease-level discounted cash flow valuation. Valuing complex office, retail, and industrial properties typically requires granular lease-by-lease cash flow projections, which ARGUS handles with institutional-grade precision. Lenders, appraisers, and major investment partners explicitly mandate .argus file formats for compliance and verification.

However, this standardization comes at a severe financial and operational cost. ARGUS Enterprise is fundamentally a mathematical modeling engine, not a document processing pipeline, deal management tool, or development pro forma tool. Its architecture is notoriously rigid, requiring extensive manual data entry to populate the models. Furthermore, it is a highly expensive commercial platform. Seat licenses typically command $1,500 per user per month, with enterprise deployments scaling between $15,000 and $25,000 annually per user.

The structural failure of off-the-shelf tools like ARGUS is that they are built to accommodate the 80 percent of standardized commercial assets. When an acquisition firm's competitive edge relies on specialized, contrarian strategies—such as acquiring distressed Class B office space for conversion into life science laboratories or high-density residential housing—the standard software templates completely collapse. Analysts are forced to spend upwards of 15 hours manually pulling non-standard comparables, factoring in highly specialized tenant improvement allowances, and building complex, error-prone Excel models from scratch.

At a typical institutional deal pace of 10 to 15 offering memorandums (OMs) per week, a financial analyst spends 20 to 30 minutes per deal purely on manual data entry before they can even make a preliminary "kill" decision. This translates to 4 to 6 hours per week of highly skilled, highly compensated labor wasted entirely on administrative transcription.

The AI-Native Underwriting Architecture

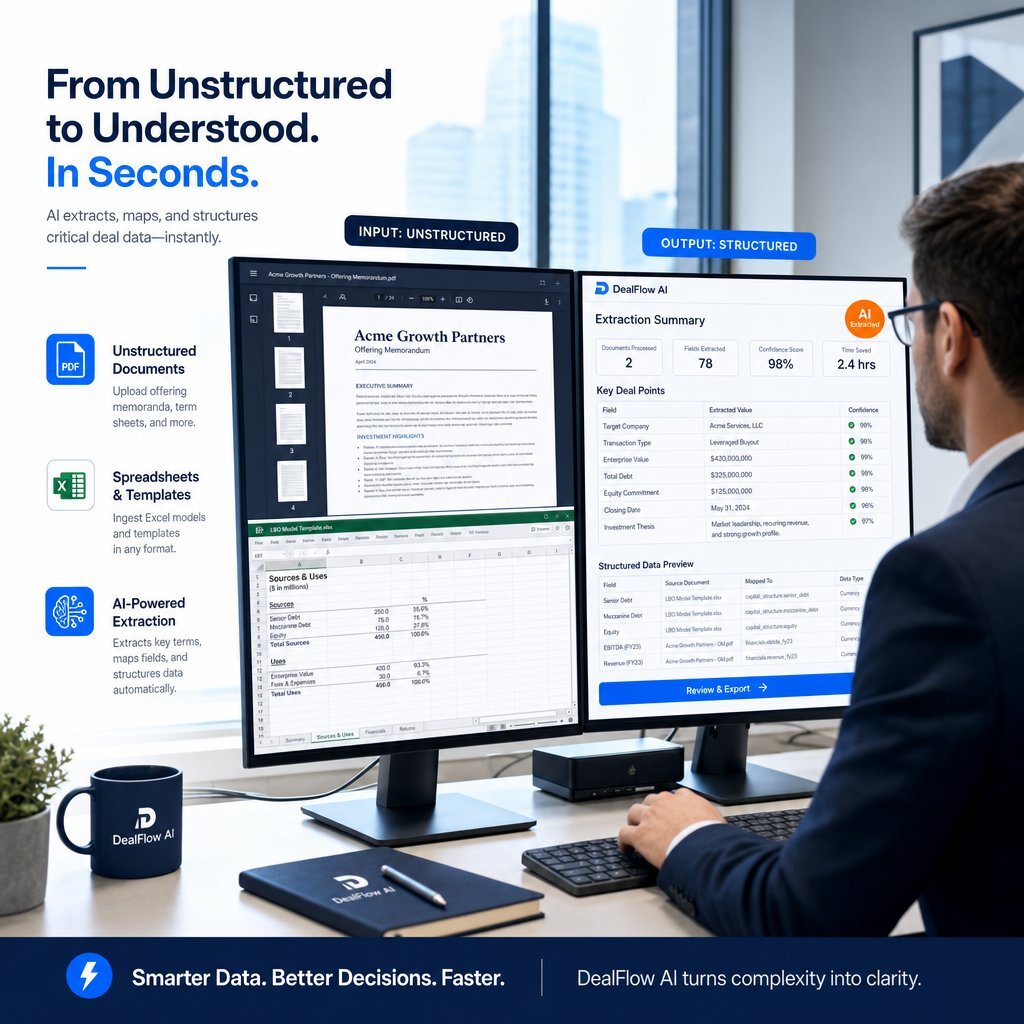

Custom software explicitly designed for real estate financial modeling solves this exact bottleneck through advanced document intelligence. Artificial intelligence-native platforms—ranging from custom builds to specialized tools like Apers, RedIQ, and Dealpath—now generate complete, working financial models directly from unstructured deal documents in minutes.

A modern custom valuation architecture typically utilizes application programming interfaces (APIs) from top-tier large language models (such as Claude 4.6 or GPT-5.4) connected to scalable databases like Supabase. This system parses unstructured PDFs, offering memorandums, rent rolls, and trailing twelve-month (T12) operating statements with unprecedented accuracy. The intelligence engine extracts the relevant financial data, reconciles conflicts between different source documents, and maps the structured data directly into the firm’s proprietary Excel templates.

The speed advantage generated by this architecture is staggering. A human analyst manually entering a 200-unit multifamily rent roll into a financial model requires 4 to 6 hours; a custom artificial intelligence application executes the extraction, structuring, and categorization in approximately 30 seconds. For a complex office offering memorandum with 15 highly variable leases, AI extraction takes roughly 45 seconds compared to 2 to 3 hours of manual transcription.

| Underwriting Task | Legacy Manual Processing | Custom AI-Automated Processing | Efficiency Gain |

|---|---|---|---|

| 200-Unit Multifamily Rent Roll | 4 to 6 hours | 30 seconds | >99% reduction |

| Complex Office OM (15 Tenants) | 2 to 3 hours | 45 seconds | >99% reduction |

| Retail Center (40 Tenants + CAM) | 6 to 8 hours | 60 seconds | >99% reduction |

| Document Reconciliation | Manual side-by-side review | Automated flagging of anomalies | Extremely High |

Data synthesized from industry software benchmarks comparing traditional entry to AI extraction.

The Complexity of Mixed-Use Underwriting

The payback of custom artificial intelligence is particularly pronounced in complex, mixed-use acquisitions. Traditional mixed-use underwriting is notoriously slow and prone to errors because residential rent rolls and commercial lease abstracts reside in entirely different document formats and possess fundamentally different economic structures. Analysts must manually extract the residential data from unit-level schedules, abstract the commercial leases by hand, and run two separate market research workflows to validate benchmark rents for multifamily versus retail spaces. Finally, they must manually consolidate two distinct income streams with entirely different expense structures into a single net operating income (NOI) model, frequently resulting in formulaic errors.

Purpose-built acquisition software automates this entire sequence. The technology extracts both the residential rent roll data and the commercial lease abstractions from the same broker package simultaneously. It validates each income stream against its respective market benchmarks and automatically builds a consolidated NOI model that appropriately flags when residential and commercial components require different capitalization rate treatments for valuation.

The Quantifiable ROI in Underwriting

The return on investment for custom valuation software is undeniable. By reducing the time spent on manual data entry and initial market research from 8 hours per week to 2 hours, an analyst recovers 24 hours of productive capacity per month. At a fully loaded cost of 50 to 80 per hour for a skilled financial analyst, the technology yields 1,200 to 1,920 in direct monthly savings per user. This represents a 10x to 20x return on investment within the first month of deployment. Furthermore, industry research indicates that leading institutional buyers leveraging artificial intelligence in real estate decision-making report 23 percent faster transaction times and 18 percent more accurate valuations, effectively compressing bid cycles from weeks to days. For firms that want to turn these time savings into a structured execution plan, pairing this underwriting work with an enterprise AI implementation roadmap can help scale wins quickly and safely.

The Leasing Pipeline and CRM Architecture: Accelerating Speed to Revenue

Beyond the acquisition phase, the second major frontier for custom commercial real estate software lies in the leasing pipeline and customer relationship management (CRM). In a market characterized by shrinking operating margins and elevated tenant expectations, the speed at which a space is leased directly impacts the asset's overall profitability.

AI-Powered Lease Abstraction

Lease abstraction—the laborious process of extracting critical dates, encumbrances, expense obligations, and renewal terms from dense legal documents—is historically one of the most tedious and error-prone tasks in commercial real estate. A human analyst typically spends 2 to 3 hours abstracting a single complex commercial lease. At scale, across a portfolio of 1,000 or more leases, this represents an enormous labor burden that frequently results in inconsistent data and missed critical dates.

Modern asset management platforms and specialized tools like Prophia or LeaseLens utilize artificial intelligence to instantly read, abstract, and structure lease data. The technology identifies key clauses and financial obligations across dozens of pages and historical amendments in a single pass. By automating this process, the productivity gain is equivalent to adding one to two full-time analysts to a firm's staff. Real-time stacking plans, encumbrance tracking, and critical date alerts are generated automatically, optimizing the landlord's ability to drive conversions, track lease expirations, and manage the deal pipeline without manual oversight.

The Evolution of the Renter-Centric CRM

Legacy CRM systems in real estate often functioned as little more than glorified, static address books. In contrast, modern custom CRM architectures act as the central nervous system for the leasing lifecycle. Platforms like VTS in the commercial sector, or Funnel Leasing and Knock in the multifamily sector, centralize operations, automate routine work, and deeply integrate with underlying property management software to remove fragmented inefficiencies.

The architectural design of these next-generation platforms fundamentally changes how leads are managed. Instead of treating every individual property within a portfolio as an isolated data silo, advanced systems employ a "renter-centric" architecture. A single, centralized guest card follows a prospective tenant from their initial inquiry, through the touring phase, to the signed lease, and eventually through the renewal process—even if they transfer between different properties owned by the same holding firm. This unified data model prevents duplicate entries, enables sophisticated cross-selling between communities, and dramatically lowers back-office labor costs.

Deflecting the Administrative Burden

Labor costs represent a primary target for operational optimization. Modern commercial and multifamily CRMs automatically execute lead scoring, direct routing to appropriate agents, follow-up communications, and automated tour scheduling. Integration with generative artificial intelligence allows virtual leasing assistants to handle prospect inquiries across chat, email, voice, and text on a 24/7 basis.

Industry data indicates that up to 86 percent of initial prospect inquiries can be handled autonomously via AI without any human intervention. This massive deflection of administrative burden allows onsite staff to transition away from low-value data entry and focus entirely on high-value resident interactions, relationship building, and physical property tours. Consequently, operators can shift from traditional staffing ratios toward centralized, shared-services models. A smaller, specialized team can efficiently handle inquiries for multiple properties, managing significantly more units with fewer personnel, resulting in up to 35 percent efficiency gains in leasing tasks.

Furthermore, tight bidirectional integration between the CRM and the core Property Management System (such as Yardi, RealPage, or MRI) is essential for maintaining data integrity. This integration ensures that pricing, unit availability, and concession data are perfectly synchronized in real time across all marketing channels, eliminating the costly manual reconciliation errors and miscommunications that plague disconnected systems. For owners rethinking their entire go-to-market stack, these renter-centric and shared-services patterns line up closely with the idea of an internal AI app store and orchestration hub described in Baytech’s enterprise AI app store blueprint.

Property Operations: The IoT and HVAC Energy Payback

The third domain where custom software and artificial intelligence generate irrefutable financial payback is in physical property operations and facilities management. Across real estate investment trusts (REITs) and commercial portfolios, approximately 37 percent of operational tasks possess high automation potential, pointing toward an estimated $34 billion in industry-wide efficiency gains by 2030.

Predictive Maintenance and "Zombie Assets"

Traditional property management operates on a reactive or strictly calendar-based maintenance schedule. Equipment is serviced when it breaks or when an outdated manual dictates, regardless of actual usage or condition. This antiquated approach leads to catastrophic equipment failures, exorbitant emergency repair premiums, and shortened asset lifecycles.

Custom operational software integrates Internet of Things (IoT) sensors directly with artificial intelligence analytics platforms to enable autonomous building responses. These systems continuously ingest telemetry data from mechanical infrastructure. Machine learning algorithms analyze vibration patterns, thermal outputs, and energy consumption rates to detect anomalies and flag mechanical deterioration long before a total failure occurs. Maintenance requests are automatically routed to technicians without manual intervention, drastically reducing emergency repair costs and extending equipment life.

By marrying operational technology with financial platforms, owners gain profound visibility into the total cost of ownership for physical assets. Standard computerized maintenance management systems (CMMS) present a deeply flawed picture of repair costs. A standard system might record a 200 labor charge and a 50 parts charge, concluding a repair cost of $250. However, advanced custom platforms integrate Overall Equipment Effectiveness (OEE) and downtime data. If an asset’s downtime halts significant commercial activity—for example, an HVAC failure in a critical lab space or a production line—the true cost of that failure is exponentially higher. Software that fails to integrate downtime data underestimates true asset costs by up to 90 percent, allowing "Zombie Assets" to drain profitability unnoticed.

Energy Optimization and the Bottom Line

Energy consumption represents one of the largest controllable operating expenses on a commercial property's income statement. The payback for optimizing this expense is immediate, quantifiable, and drops directly to the net operating income line, instantly boosting the asset's capitalized value.

Advanced software platforms optimize heating, ventilation, and air conditioning (HVAC) systems dynamically. Instead of relying on static temperature setpoints, AI-driven systems adjust HVAC loads in real time based on building occupancy levels, granular foot traffic patterns, time of day, and external weather conditions. In a documented case study of a Class A office tower, the implementation of IoT sensors combined with AI-driven setpoint optimization resulted in a massive 28 percent reduction in total HVAC energy costs. This holistic operational intelligence provides the undeniable business case for upgrading legacy building management systems.

These same operational data streams and controls are exactly the type of high-value, latency-sensitive workloads that benefit from a thoughtful deployment choice between edge and on-prem environments. As leadership teams weigh these options, resources like Baytech’s edge vs. on‑prem AI guide can help align building automation and energy projects with the right underlying infrastructure.

The Dark Side of AI: Security, Compliance, and the Liability Trap

While the financial upside of custom software in underwriting, leasing, and operations is highly documented, the deployment of artificial intelligence carries severe, frequently overlooked risks. The primary danger zone lies in the utilization of generic, consumer-tier artificial intelligence platforms to process highly confidential commercial real estate data.

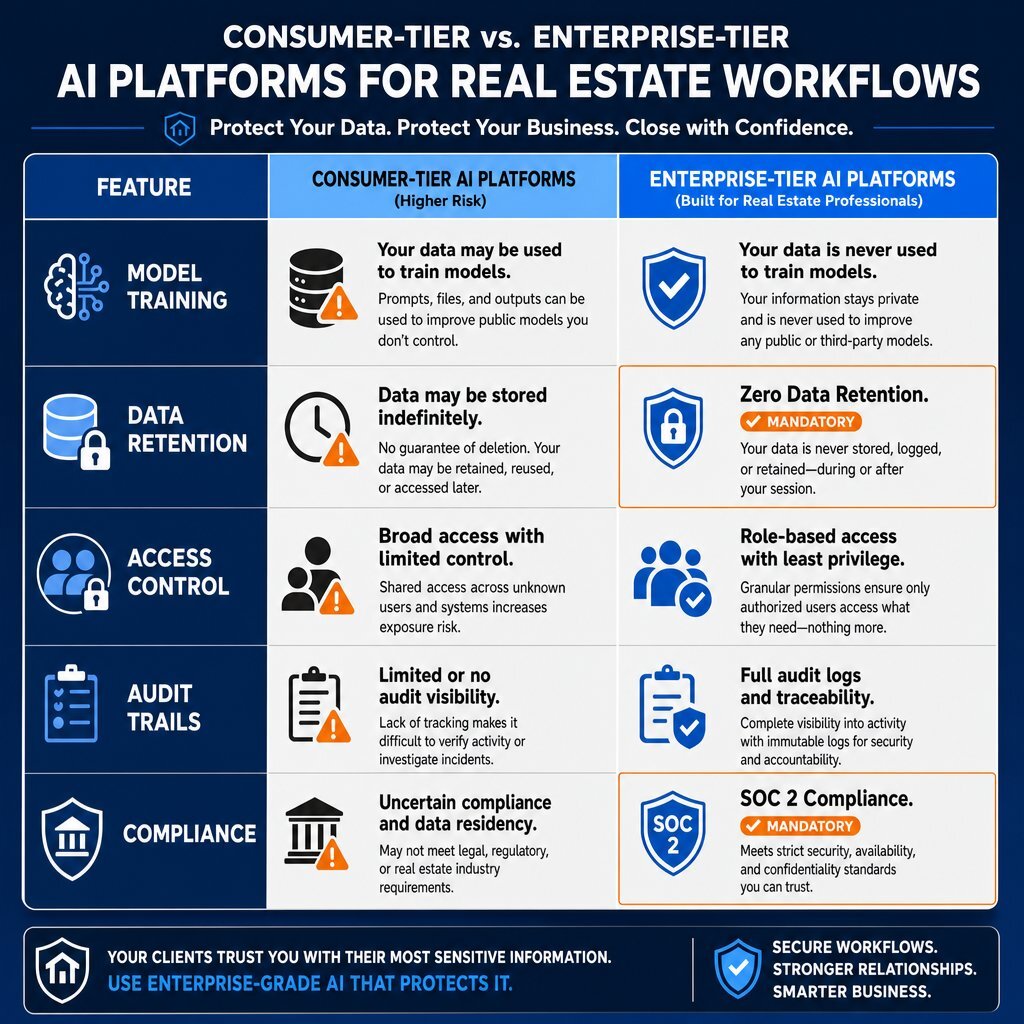

The Consumer vs. Enterprise AI Divide

Commercial real estate transactions involve some of the most sensitive financial and personal data in the global economy. Analysts routinely process unredacted rent rolls containing personally identifiable information (PII), proprietary purchase agreements, non-public corporate financials, and confidential loan documents.

A widespread and catastrophic error made by many real estate professionals is utilizing consumer-tier artificial intelligence subscriptions—such as ChatGPT Plus, Claude Pro, or Gemini Advanced, which typically cost $20 per month—for deal analysis and document summarization. The distinction between consumer and enterprise-grade AI is not a matter of computational capability; the underlying foundational models are often identical. The difference is entirely a matter of legal liability, data privacy, and security architecture.

Consumer-tier AI models are governed by non-negotiable click-wrap terms of service. By default, these platforms frequently retain user input for a minimum of 30 days for safety reviews. Crucially, they may use the inputted data to train and improve their future commercial models unless a user proactively navigates the settings to opt out. Entering an unredacted rent roll or a confidential joint venture agreement into a consumer AI model represents a direct, actionable violation of standard non-disclosure agreements and fiduciary obligations.

Enterprise-tier plans—such as ChatGPT Enterprise, Claude for Work, or Gemini Enterprise, which typically cost 30 to 60 per user per month—provide the mandatory contractual and technical safeguards required for institutional real estate. The critical differentiators include:

- Zero Data Retention (ZDR): This is the strongest security posture available, wherein inputs and outputs are not stored or persisted on the vendor's infrastructure beyond the milliseconds required to return a response. This is essential for processing PII and loan documents.

- Exclusion from Model Training: Enterprise plans provide explicit contractual guarantees within signed Data Processing Agreements (DPAs) that customer data will never be used to train the vendor's models.

- SOC 2 Type II Certification: These platforms undergo independent third-party audits confirming they meet rigorous standards for security, availability, processing integrity, and privacy.

- Administrative Governance: Single Sign-On (SSO) and SCIM provisioning allow administrators to instantly revoke access if an employee departs the firm, preventing the exfiltration of sensitive deal data. Furthermore, enterprise plans maintain immutable audit logs of user activity, which are critical for passing risk committee reviews, answering regulatory inquiries, and surviving lender due diligence.

When AI vendors lack these enterprise-grade features, deals stall. Risk committees and examiners demand provenance, not a black box operating on shared infrastructure where data cross-contamination is possible.

| Feature / Requirement | Consumer AI Tier ($20/mo) | Enterprise AI Tier (30-60/mo) | Strategic CRE Regulatory Implication |

|---|---|---|---|

| Model Training | May use inputs for training | Contractually excluded via DPA | High risk of NDA breach if consumer tier used |

| Data Retention | Stored for 30+ days | Zero Data Retention (ZDR) available | Fiduciary compliance for PII and financials |

| Access Controls | Individual personal accounts | SSO / SCIM provisioning | Immediate offboarding required for departed staff |

| Audit Trails | None | Immutable logs maintained | Required for risk committee and examiner reviews |

| Compliance standard | Terms of Use (Click-wrap) | SOC 2 Type II, Signed DPA | Mandatory for institutional LP onboarding |

Table: AI Security Posture and Compliance Distinctions for Real Estate Workflows.

The Colorado AI Act: The New Paradigm of Algorithmic Liability

The regulatory environment surrounding artificial intelligence in real estate is rapidly hardening, shifting from theoretical risk to statutory liability. The most significant development in 2026 is the passage of Colorado Senate Bill 26-189, which repeals and replaces the 2024 Colorado AI Act. Taking effect on January 1, 2027, this legislation establishes a stringent, targeted framework regulating the use of "automated decision-making technology" (ADMT) in consequential decisions.

Crucially for the commercial real estate sector, the law explicitly classifies "leasing or purchasing residential real estate" as a covered domain. An ADMT is defined broadly as technology that processes personal data and uses computation to generate outputs—such as predictions, classifications, or tenant risk scores—used to make or assist decisions. If an automated system's output materially influences a consequential decision regarding a lease or property purchase, the deployment of that system is heavily regulated by the state.

The regulatory burden placed on real estate deployers (landlords, property managers, and brokerage firms) is immense and unprecedented. Under the law, deployers must provide clear and conspicuous pre-decision notice to consumers that an automated system is being utilized to evaluate their application. Furthermore, if the AI system results in an "adverse outcome"—such as the denial of a lease application or the offering of materially worse pricing terms or higher deposits—the deployer must provide a detailed disclosure within 30 days.

This mandatory disclosure must explain in plain language the specific role the technology played in the denial, and it must inform the consumer of their statutory right to request a "meaningful human review" of the decision.

The Death of the Black Box

This legislation effectively prohibits automated systems from operating as unaccountable black boxes. Consumers possess the right to demand that a trained human with the authority to override the system reviews the evidence and the algorithmic output. The human reviewer must understand the system's inputs and limitations and cannot simply default to the automated output.

Furthermore, the law directly addresses algorithmic discrimination. In cases where an ADMT-influenced real estate decision violates existing anti-discrimination statutes (such as the Colorado Anti-Discrimination Act or federal fair housing laws), liability is apportioned between the software developer and the real estate deployer based on relative fault. Contracts that attempt to blanket-indemnify a developer or deployer against their own discriminatory acts are rendered legally void.

This legislative framework demonstrates exactly why custom, fully transparent software architectures are becoming mandatory. Real estate firms can no longer blindly deploy off-the-shelf algorithmic tenant screening tools if the vendor cannot clearly explain how the model weighs specific variables. The inability to produce a clean audit trail, access the underlying data points, or explain the decision logic directly exposes the real estate firm to state-level enforcement actions by the Attorney General. The Bounded Buy strategy, which ensures a firm owns and understands its differentiating logic, acts as a critical shield against this new wave of algorithmic liability. For organizations building or buying agentic systems to automate underwriting or leasing workflows, patterns like scoped permissions and human-in-the-loop controls—outlined in Baytech’s guidance on securing agentic AI—are quickly becoming non‑negotiable.

Conclusion: The 2026 Strategic Playbook

The commercial real estate landscape of 2026 demands relentless operational efficiency to offset high capital costs, massive debt maturities, and bifurcating asset values. Artificial intelligence is no longer a speculative concept or a marketing buzzword; it is the fundamental delivery mechanism for the highest-value analytical and operational work in the industry. The gap between firms deploying custom AI architectures and those relying on legacy manual workflows is now measured in months, not percentage points.

However, the technology only pays back when applied with extreme precision to areas of massive labor friction: extracting and structuring unstructured lease data in seconds, generating complex financial models instantly to compress bid cycles, centralizing fragmented CRM pipelines to reduce onsite headcount, and autonomously optimizing building HVAC infrastructure to drive down energy costs. When targeted accurately, the returns are immense—recovering thousands of hours of analyst capacity, reducing energy consumption by double digits, and deflecting the vast majority of routine administrative inquiries.

Equally critical is understanding where the technology introduces catastrophic risk. The deployment of consumer-grade artificial intelligence for proprietary deal analysis is a severe breach of data security and fiduciary duty. Concurrently, the use of opaque, off-the-shelf algorithmic tools for tenant screening exposes firms to profound legal liability under stringent new legislative frameworks like the Colorado AI Act.

Ultimately, the most successful commercial real estate firms in 2026 abandon the monolithic build-versus-buy debate. By adopting the Bounded Buy architectural strategy, leaders secure standardized utility software off the shelf while aggressively building custom, AI-native differentiators. This disciplined approach ensures that technology investments yield defensible competitive advantages, turning structural market complexities into quantifiable, undeniable operational outperformance. And as AI infrastructure, pricing, and SaaS markets continue to shift, aligning this strategy with a portability-first, portability-focused AI roadmap helps CRE owners and operators protect margins, data, and long-term flexibility.

About Baytech

At Baytech Consulting, we specialize in guiding businesses through this process, helping you build scalable, efficient, and high-performing software that evolves with your needs. Our MVP first approach helps our clients minimize upfront costs and maximize ROI. Ready to take the next step in your software development journey? Contact us today to learn how we can help you achieve your goals with a phased development approach.

About the Author

Bryan Reynolds is an accomplished technology executive with more than 25 years of experience leading innovation in the software industry. As the CEO and founder of Baytech Consulting, he has built a reputation for delivering custom software solutions that help businesses streamline operations, enhance customer experiences, and drive growth.

Bryan’s expertise spans custom software development, cloud infrastructure, artificial intelligence, and strategic business consulting, making him a trusted advisor and thought leader across a wide range of industries.