Why Generic AI Startups Are Dead: Playbook for Moats

March 04, 2026 / Bryan Reynolds

VCs Say Generic AI SaaS Startups Are Now Unfundable: The Executive Guide to Defensibility, Moats, and Custom AI Integration

Venture capitalists are no longer treating “AI-powered” as a pitch-deck cheat code. In recent conversations with the investment community, a definitive and uncompromising message has emerged: a rapidly growing share of artificial intelligence software-as-a-service (SaaS) startups—especially those built as thin workflow layers on top of large language models—have become effectively unfundable.

This monumental shift, heavily detailed in recent industry reporting, reflects a market that has violently transitioned from an era of unbridled experimentation to one of rigorous, structural defensibility.

Investors assert that the unprecedented ease of building and cloning AI products has entirely collapsed the competitive advantage that once stemmed from slick user interfaces and basic task automation. Consequently, this dynamic is forcing technology startups and established enterprise software vendors alike to prove they possess assets that are fundamentally harder to copy: proprietary data flywheels, owned distribution channels, or deep integration into mission-critical workflows.

For executives at B2B firms—spanning advertising, gaming, real estate, finance, education, telecommunications, high-tech, and healthcare—understanding this venture capital recalibration is not merely an academic exercise; it is a strategic imperative. The tools and platforms that organizations choose to procure, build, or invest in today must survive the rapid commoditization of foundational intelligence. This comprehensive report deconstructs the macroeconomic funding landscape, the collapse of the "thin wrapper" business model, the precise operational metrics investors now demand, and the strategic mandate for custom enterprise software development.

The Macroeconomic Venture Climate: A Tale of Two Markets

The venture capital ecosystem in 2025 and early 2026 presents a striking paradox. On a macroeconomic level, global venture funding is surging, driven almost exclusively by the artificial intelligence sector. In 2024, AI companies captured over $100 billion, representing approximately 33% of all global venture funding—a staggering 80% year-over-year growth compared to 2023.

As the market advanced into 2025, this concentration intensified dramatically. By the close of 2025, the AI sector had absorbed $202.3 billion, capturing nearly 50% of all global startup funding.

However, beneath these headline-grabbing figures lies a brutal reality for application-layer software companies. The capital deployed is not distributed evenly. The mega-rounds of 2024 and 2025 were heavily concentrated in foundation model developers (such as OpenAI, Anthropic, and xAI) and the critical infrastructure required to run them (compute, data centers, and semiconductor optimization).

For traditional SaaS companies and generic AI applications, the funding environment has reached crisis levels. Industry analysts have dubbed this phenomenon the "SaaSpocalypse," noting that traditional B2B SaaS funding dropped significantly as enterprise IT budgets were aggressively reallocated toward AI agents and orchestration tools.

Consequently, investors are drawing absolute red lines. Applications that merely add a chat interface to an existing Large Language Model (LLM) are receiving immediate passes from leading venture firms. The market is now demanding businesses that can exhibit both the hyper-growth of an AI-native product and the durable, highly defensible unit economics of a legacy enterprise software giant.

The AI-Native Valuation Premium

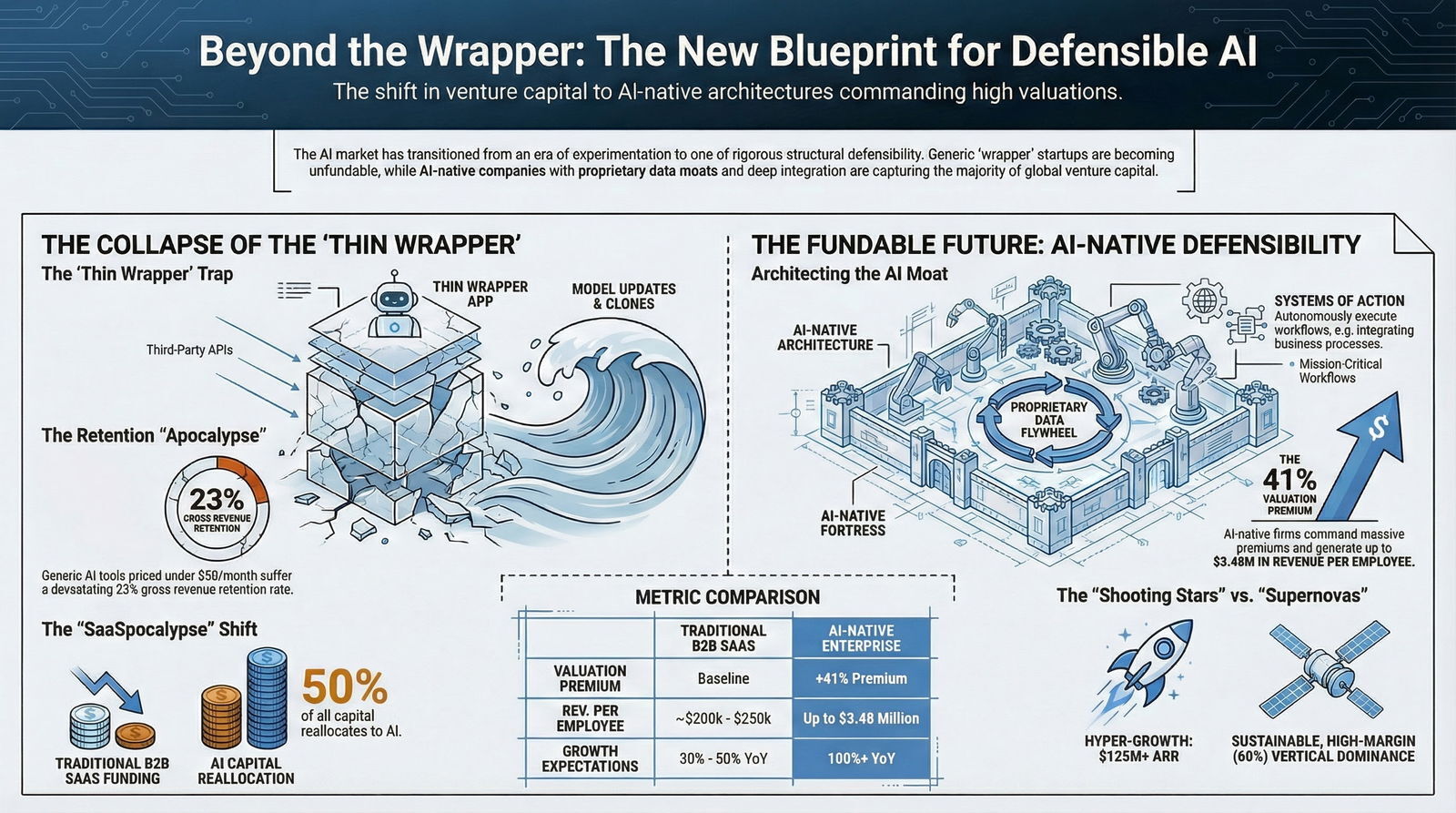

The bifurcation of the software market has resulted in a massive valuation premium for genuinely defensible, AI-native organizations. Startups characterized as "AI-native"—meaning AI is the core architectural foundation rather than a bolted-on feature—command a valuation premium of up to 41% over their non-AI counterparts.

Furthermore, these companies are demonstrating remarkable operational leverage, often achieving revenue per employee metrics that are six times higher than traditional SaaS benchmarks.

| Market Metric | Traditional B2B SaaS | AI-Native Enterprise SaaS | Source / Implication |

|---|---|---|---|

| Share of Global VC (2025) | Shrinking (Less than 20%) | ~50% ($202.3 Billion) | AI absorbs a disproportionate amount of capital. |

| Valuation Premium | Baseline | +41% Premium | High demand for core AI architecture. |

| Revenue per Employee | ~200k - 250k | Up to $3.48 Million | AI enables massive operational leverage. |

| Growth Expectations | 30% - 50% YoY | 100%+ YoY | VCs expect hyper-growth from AI investments. |

Data derived from Bessemer Venture Partners State of AI 2025 and comprehensive industry SaaS benchmarks.

The Collapse of the "Thin Wrapper" Architecture

To comprehend why venture capitalists have turned hostile toward generic AI startups, it is vital to dissect the architecture of the "thin wrapper." A thin wrapper is defined as an application whose core functionality relies almost entirely on third-party foundation models via API calls, without adding significant proprietary logic, unique data ingestion, or deep workflow integration.

The Illusion of First-Mover Advantage

In 2023, during the initial generative AI boom, speed to market was viewed as a viable strategy. Startups that rapidly wrapped APIs in polished user interfaces to write marketing copy, generate code, or summarize legal documents experienced explosive early user adoption. However, this growth proved fundamentally fragile. The critical flaw of the thin wrapper is that its primary competitor is not necessarily other agile startups, but the foundation model providers themselves.

Every time a frontier model provider expands its context window, introduces native multimodality, or launches autonomous file analysis capabilities, entire sub-categories of wrapper startups are rendered obsolete overnight. If an AI product's core value proposition is easily matched by a native feature update from OpenAI, Google, or Anthropic, that product inherently lacks a sustainable business moat.

The Threat of Prompt Portability and "Vibe Coding"

Venture capitalists note that basic UI polish and light task automation are now considered mere table stakes. The barrier to software prototyping has dropped to near zero. Through the emerging trend of "vibe coding"—natural language-driven software development where founders simply describe the application they want built to an AI coding assistant—competitors can clone generic AI applications in a matter of days.

When competitive differentiation relies solely on "better prompts" or a slightly cleaner dashboard, the resulting business model is structurally flawed. Prompts are highly portable, and generic workflow logic is easily reverse-engineered. Investors clearly recognize that if an API key and a small team using an AI coding agent can replicate a startup's core product over a weekend, that startup does not possess a venture-backable business; they possess a temporary arbitrage opportunity that is rapidly closing.

The Margin Squeeze and Unit Economics

A primary, non-negotiable dealbreaker for investors in 2026 is an unsustainable gross margin profile driven by AI inference costs. Foundation models are computationally expensive to query. Startups that subsidize heavy user engagement without a clear path to profitability quickly burn through their venture capital.

Investors are implementing rigorous assessments of unit economics, specifically demanding a clear path where Customer Lifetime Value (LTV) significantly exceeds Customer Acquisition Costs (CAC), typically at a ratio of 3:1 or higher. If an AI tool is treated as a generic utility, users will invariably flock to the cheapest provider, triggering a race to the bottom. Companies whose products cost more to operate in API inference fees than customers are willing to pay in subscription revenue are actively categorized as unfundable.

Modern AI-native teams are also expected to control those costs with techniques like model routing, prompt compression, and semantic caching to avoid what some call the “token tax” of LLMs. Without this kind of engineering discipline, even clever products can see their margins evaporate in real time.

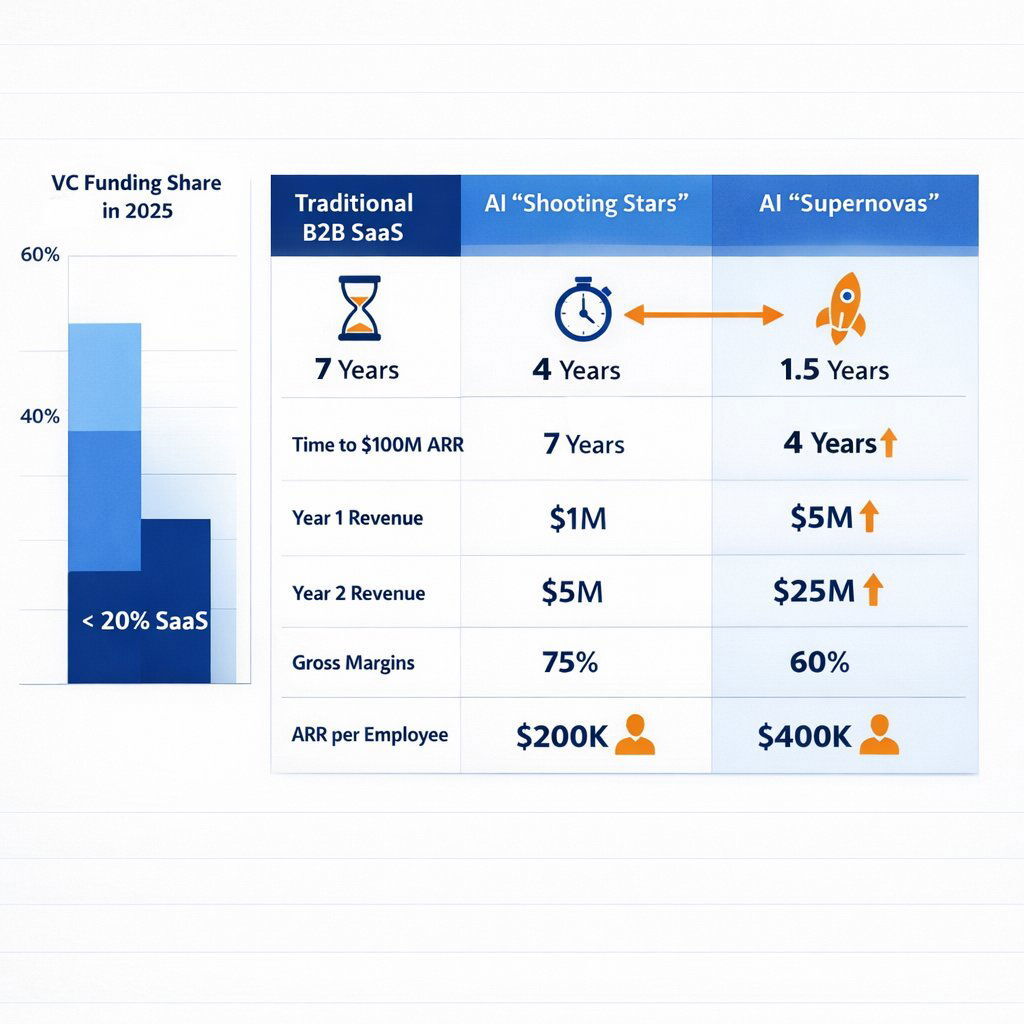

Benchmarking the New Elite: Supernovas vs. Shooting Stars

To quantify what a fundable AI startup looks like in the current climate, the venture capital industry relies on rigorous, updated benchmarking. The authoritative State of AI 2025 report published by Bessemer Venture Partners (BVP) categorized the breakout AI companies into two distinct, highly successful archetypes: "Supernovas" and "Shooting Stars". These benchmarks highlight the dual paths to unicorn status in the modern SaaS era.

The AI Supernova Archetype

Supernovas represent explosively scaling AI startups experiencing unprecedented adoption rates, often driven by intense consumer or broad enterprise demand.

- Revenue Velocity: They achieve approximately $40 million in Annual Recurring Revenue (ARR) in their first year of commercialization, and scale to a staggering $125 million by year two.

- Unit Economics: This hyper-growth comes at a severe cost. Supernovas typically operate with fragile retention metrics and incredibly thin gross margins—averaging around 25%, and often operating at negative margins—as they aggressively buy market share in winner-take-all categories.

- Efficiency: Despite the low margins, they boast extreme operational efficiency, generating an astounding $1.13 million ARR per full-time employee (ARR/FTE), heavily relying on AI for their own internal operations.

The AI Shooting Star Archetype

Shooting Stars emulate the trajectory of stellar, highly efficient traditional B2B SaaS companies, but their growth is accelerated by AI-native architectures and proprietary data moats.

- Revenue Velocity: They reach approximately $3 million ARR in year one, quadruple to 12 million by year two, and surpass the 100 million ARR threshold by year four.

- Unit Economics: Unlike Supernovas, these companies boast strong product-market fit with healthy, sustainable gross margins hovering around 60%.

- Efficiency: They generate a solid $164k ARR/FTE in their first year, growing sustainably while maintaining incredibly loyal enterprise customer bases with high switching costs.

The Implication for Generic SaaS

For a generic AI SaaS startup, the implications of these benchmarks are severe. Failing to meet the operational discipline and high margins of a Shooting Star, or the raw, explosive velocity of a Supernova, renders a company effectively unfundable. VCs now demand either highly defensible, high-margin vertical dominance, or world-altering hyper-growth.

A traditional SaaS company growing from 20 million to 35 million in ARR (a highly respectable 75% growth rate) is now considered virtually unfundable by top-tier venture funds if it lacks a core AI architectural advantage.

| Financial Benchmark | Traditional Top-Quartile SaaS | AI "Shooting Stars" (Defensible B2B) | AI "Supernovas" (Hyper-Growth) |

|---|---|---|---|

| Time to $100M ARR | ~7 Years | ~4 Years | ~1.5 Years |

| Year 1 ARR | < $1M | ~$3M | ~$40M |

| Year 2 ARR | ~2M - 3M | ~$12M | ~$125M |

| Average Gross Margin | 75% - 85% | ~60% | ~25% (Often negative) |

| ARR per Employee | ~200k - 250k | ~$164k (Year 1) | ~$1.13M |

Data derived from Bessemer Venture Partners State of AI 2025 and comprehensive industry SaaS benchmarks.

Architecting the AI Moat: Data, Distribution, and Workflows

If generic wrappers are unfundable, what exactly are venture capitalists looking to finance? The answer lies in structural defensibility. Renowned investor Warren Buffett historically defined a moat as a business's ability to protect long-term profits and market share from competitors.

In the age of AI, the foundational algorithm itself is no longer the moat; rather, it is the infrastructure, proprietary data, and deeply embedded workflows built around the model that secure lasting competitive advantage.

1. Proprietary Data Flywheels

The most critical asset an AI startup can possess is a unique dataset that horizontal foundation models cannot easily access via public web scraping. However, merely possessing static proprietary data is insufficient. The true moat is an active "data flywheel"—a closed-loop system where continuous user interactions naturally generate proprietary feedback.

Every time a user corrects an AI-generated output, accepts a predictive recommendation, or inputs an industry-specific edge case, the system must capture that data to fine-tune the underlying model. This creates a compounding advantage: the product becomes demonstrably smarter with scale, which inherently attracts more users, which in turn generates richer data.

This dynamic explains why vertical AI platforms that capture highly sensitive medical records, bespoke legal contracts, or complex industrial logistics data are incredibly defensible. Open-source competitors and generic models simply cannot recreate the nuanced context required to train equivalent systems.

2. Workflow Ownership and Systems of Action

For the past decade, enterprise software was defined by "Systems of Record"—platforms designed primarily to store information, such as a Customer Relationship Management (CRM) database.

Artificial intelligence is actively forcing a paradigm shift toward "Systems of Action."

Investors are aggressively seeking platforms that do not merely store information or serve as passive human assistants, but actively and autonomously execute complex tasks. Agentic AI frameworks can fetch real-time insights, trigger operational actions, and complete end-to-end multi-step business processes without a human continually clicking through a user interface.

By owning the entire workflow from initiation to resolution, the software becomes deeply embedded into the daily, mission-critical operations of an enterprise. This deep integration creates massive structural switching costs. Ripping out an AI agent that inherently understands a company's internal supply chain routing is a monumental, highly disruptive operational decision; conversely, canceling a $20-per-month subscription to a generic marketing copy chatbot requires zero deliberation.

Many leaders are now exploring goal-driven, multi-agent “teams of bots” that can manage these workflows end to end, rather than relying on a single chatbot. Approaches like this—often called agentic AI systems—are what turn simple assistants into true Systems of Action.

3. The Dominance of Distribution

In a technological era where the financial and technical cost of building a minimum viable product (MVP) is approaching zero, distribution remains the ultimate battlefield.

A superior product with weak visibility will inevitably lose to an inferior product backed by massive distribution momentum.

Startups that can establish industry trust, secure strategic go-to-market partnerships, and dominate search and AI-driven discovery visibility create an acquisition moat that is incredibly difficult for new entrants to penetrate.

As one investor bluntly noted, momentum is the new moat; securing mindshare and starving competitors of oxygen is paramount before they can leverage AI tools to clone the feature set.

Industry-Specific Defensibility: Vertical AI in Action

The mandate for B2B executives is clear: shift from horizontal, generalized platforms to vertical, highly specialized solutions. By focusing on deep, industry-specific workflows, organizations can build products and internal tools that general-purpose AI models cannot safely or legally emulate. Below is a detailed analysis of how defensibility is currently being established across major enterprise sectors.

Advertising and Marketing

The advertising sector is witnessing a massive influx of AI designed to deliver hyper-personalization at unprecedented scale.

However, the competitive moat is no longer the generation of ad copy or basic image creation—LLMs execute this natively and cheaply. The true moat lies in "representation learning" and deep predictive analytics.

Defensible marketing platforms centralize a brand's complex understanding of its customers, successfully connecting disparate data points (such as matching online browsing behavior with localized in-store inventory patterns) to orchestrate automated, cross-channel campaigns.

When an AI system becomes the central intelligence engine managing millions of dollars in programmatic ad spend, replacing it is viewed by the Chief Marketing Officer as an unacceptable operational risk.

Gaming and Entertainment

In the video game and entertainment sectors, the capital cost of content creation continues to rise exponentially.

Startups are building robust moats by embedding AI directly into proprietary game engines to procedurally generate immersive environments, automate 3D asset creation, and dynamically manage non-player character (NPC) behavior.

The moat is firmly established when the AI tool becomes an indispensable, integrated part of a studio's core development pipeline, significantly reducing time-to-market for AAA titles while simultaneously increasing average revenue per user through highly personalized, adaptive gameplay.

Real Estate and Mortgage Lending

The real estate and mortgage sectors suffer from notoriously labor-intensive, heavily regulated administrative workflows. AI companies in this vertical are moving far beyond generic customer service bots. Defensible platforms are actively automating complex property management processes, from real-time prospect communications to exhaustive lease audits and predictive maintenance scheduling.

True defensibility in this vertical is achieved by successfully navigating complex financial regulations and achieving deep API integrations with legacy property management software. A generic AI wrapper cannot legally underwrite a mortgage or safely navigate Fair Housing Act guidelines without specialized training, rigorous guardrails, and industry certification.

Finance and Fintech

Financial institutions operate under the most strict regulatory and compliance frameworks in the global economy, making the deployment of generic, "black box" AI tools a massive liability. Successful AI startups in the finance vertical are building their moats through highly secure, often on-premise integrations, and by developing specialized models for real-time fraud detection and portfolio risk management.

For instance, AI systems designed to analyze localized financial crime operations or parse unstructured corporate lending data create immense switching costs because they must be rigorously certified, explainable, and continuously audited.

A thin wrapper built on a public API simply cannot pass a major banking compliance audit.

Education and Learning Management Systems (LMS)

Education technology is evolving rapidly past simple essay generation and basic grading tools. The highly defensible businesses in this sector are building personalized AI tutoring systems and comprehensive workflow automation tools designed specifically for educators.

By analyzing a student's historical performance data across an entire academic semester, these systems can adapt curriculums and learning paths in real-time. The structural moat consists of the accumulation of historical learning data and the deep, seamless integration directly into the school district's entrenched Learning Management System (LMS).

Telecommunications

Telecommunications operators are grappling with the immense challenge of managing incredibly complex, dynamic network infrastructures. AI startups securing venture funding in this space are building "Agentic AI frameworks" tailored for autonomous network operations.

These advanced systems proactively identify network faults, optimize bandwidth dynamically based on real-time traffic, and support ultra-low-latency edge computing without requiring manual, human intervention.

Defensibility here is deeply rooted in proprietary integration with specific telecommunication hardware and access to highly complex network topography data.

Software and High-Tech

Within the software development industry itself, AI is moving from standard code-completion copilots to autonomous engineering agents. Defensible tools in this vertical are fully repository-aware; they understand a company's unique coding standards, track historical technical debt patterns, and integrate directly into the Continuous Integration/Continuous Deployment (CI/CD) pipelines.

The AI becomes smarter as the specific engineering team uses it, accumulating institutional knowledge. Switching to a generic coding tool means losing that deeply contextualized, accumulated intelligence.

At the same time, leaders are realizing that unguided, rapid AI coding can quietly pile up risk. Without guardrails, AI-generated code can create hidden technical debt that erodes long-term value, even if it appears to speed up delivery in the short term.

Healthcare and MedTech

Healthcare represents one of the most structurally defensible verticals due to the extreme complexity of medical data and strict adherence to HIPAA compliance regulations.

Breakout startups are successfully automating clinical note-taking and highly complex medical billing and coding workflows.

These products succeed because they integrate directly into legacy Electronic Health Records (EHR) systems and utilize proprietary medical literature to deliver FDA-audited accuracy.

The data gravity in the healthcare sector is immense; once a hospital system integrates a customized AI that securely processes patient data and recovers millions in missed revenue, the barrier to entry for any new competitor becomes virtually insurmountable.

Fast-Growing Startups

For fast-growing startups seeking to disrupt incumbents, utilizing AI is no longer a differentiator; it is the baseline expectation.

To remain fundable, these companies must build AI-native architectures from day one. This involves utilizing AI not just in the product, but across their entire internal operations—automating Go-To-Market (GTM) motions, customer support, and financial forecasting—to achieve the extreme capital efficiency and Rule of 40 metrics that investors now mandate.

That usually means rethinking the entire development lifecycle, not just sprinkling AI into one feature. Many teams are now adopting an AI-native SDLC that bakes agents, human review, and automated QA into every phase so speed never comes at the cost of trust or maintainability.

The Churn Wave: Why the Enterprise Discards Wrappers

The immense urgency for establishing a defensible moat is evidenced by the massive "churn wave" currently impacting the software industry. Annual Recurring Revenue (ARR) is the bedrock of SaaS valuations because it is typically viewed as predictable, highly retained, and durable.

However, generic AI wrapper startups are currently experiencing what analysts describe as a gross retention apocalypse.

Because the switching cost between one generic LLM wrapper and another is practically zero, enterprise buyers exhibit absolutely no brand loyalty. As soon as a marginally cheaper alternative emerges, or the core LLM provider offers the feature natively, the customer immediately churns.

Furthermore, sophisticated B2B customers quickly recognize that "prompts are portable"; they can simply copy a wrapper's workflow logic and paste it into their own internal, enterprise-secured AI accounts.

Market data clearly illustrates the extreme danger of relying on low-tier wrapper models.

The data sends a definitive, undeniable signal to B2B executives and investors: pricing and business models built on low-value, high-volume generic AI tools are toxic. AI-native products priced at under $50 per month experience a devastating Gross Revenue Retention (GRR) of just 23% and a Net Revenue Retention (NRR) of 32%.

Conversely, specialized, vertically integrated AI products that solve complex B2B workflows and charge over $250 per month achieve a healthy GRR of 70% and an NRR of 85%, effectively mirroring the stability and predictability of traditional B2B SaaS.

Long-term viability requires moving aggressively upmarket, abandoning generic applications, and solving highly complex, high-value enterprise problems.

Custom Software as the Strategic Mandate

For enterprise executives and startups seeking to escape the thin-wrapper trap and build genuine defensibility, the alternative is clear: rigorous custom software development. While off-the-shelf AI modules offer alluring speed to market, they inherently lack competitive differentiation. Generic tools cannot adapt to complex existing data architectures, nor can they consistently comply with the stringent security and governance requirements of highly regulated industries.

When a company relies entirely on a generic, vendor-supported SaaS tool for its AI capabilities, that exact same tool is equally available to their closest competitors. To build a true, lasting moat, organizations must transition from merely "renting" intelligence via API calls to fully owning their AI architecture. Custom AI solutions adapt to the organization's unique, historical data patterns, preserving valuable operational context and significantly outperforming standardized models.

This is the exact paradigm where specialized technology partners, such as Baytech Consulting, deliver critical, enterprise-grade value. Specializing in custom software development and comprehensive application management, Baytech Consulting operates on the core philosophy of providing a Tailored Tech Advantage. By architecting bespoke solutions from the ground up, businesses ensure their AI capabilities are deeply, natively integrated into their proprietary systems, rather than sitting as a highly vulnerable, easily replicable layer on top.

The engineering capabilities required to build these highly defensible, agentic systems are substantial. Developing an autonomous, AI-driven enterprise platform requires deep expertise in system orchestration, data governance, and secure scalability. Baytech Consulting's approach utilizes cutting-edge, enterprise-grade technologies to achieve this. By leveraging Docker and Kubernetes for containerized, resilient scalability, Harvester HCI and Rancher for robust infrastructure management, and Postgres alongside SQL Server for highly secure, proprietary data handling, organizations can build solutions that simply cannot be cloned in a weekend hackathon.

Crucially, by executing with a Rapid Agile Deployment methodology and utilizing highly skilled, onshore engineers, the complex development process remains entirely transparent, highly iterative, and perfectly aligned with the organization's long-term strategic objectives. Custom engineering allows companies to dictate strict data governance policies, ensure absolute regulatory compliance, and build the vital, compounding feedback loops necessary to generate long-term return on investment. While the initial capital requirement for custom development exceeds that of purchasing an off-the-shelf wrapper, it ultimately pays massive dividends in intellectual property ownership and absolute structural defensibility.

Distribution Defensibility: The "They Ask, You Answer" Methodology

Even with a robust custom software architecture and a proprietary data flywheel, an AI startup or enterprise initiative cannot survive without a highly effective go-to-market engine that establishes dominant brand authority. In the modern AI era, where baseline features can be copied almost instantly, distribution and trust constitute the final remaining, unassailable moats.

For B2B technology companies, one of the most potent, proven distribution strategies is the "They Ask, You Answer" (TAYA) methodology. Pioneered by Marcus Sheridan, TAYA is a transparent, highly educational content marketing framework that operates on a remarkably simple premise: if a prospective buyer has a question, the company must answer it openly, honestly, and exhaustively on its own digital platforms.

In a modern B2B purchasing landscape where buyers complete up to 80% of their research autonomously online before ever speaking to a sales representative, educational content is the primary, indispensable driver of lead generation and customer acquisition. TAYA dictates that companies must aggressively and transparently target the "Big 5" topics that buyers inherently care about—topics that traditional marketing departments are often terrified to address publicly:

- Cost and Pricing: Openly discussing exactly what drives the price of the software up or down, and why custom solutions cost more than wrappers.

- Problems: Honestly addressing the limitations, potential implementation hurdles, or drawbacks of a specific AI solution.

- Comparisons: Objectively comparing your products directly against key competitors in the market.

- Reviews: Highlighting authentic customer experiences, including the challenges they faced.

- Best-in-Class Lists: Acknowledging the top players in the industry, even if that list includes direct rivals.

By systematically answering these difficult questions through high-quality blog posts, deep-dive video content, and comprehensive learning centers, B2B software companies build a dominant organic search presence that captures high-intent buyers.

More importantly, they establish unparalleled market trust. When an AI startup transparently explains why its custom predictive model costs more than an off-the-shelf wrapper—and honestly details the integration challenges required to deploy it—it ceases to be viewed as a mere vendor and elevates to the status of a trusted advisor.

This radical transparency significantly reduces friction in the enterprise sales cycle, accelerates closing rates, and solidifies a brand moat that algorithmic clones and generic competitors cannot possibly replicate.

Conclusion: The Path Forward for B2B Executives

The venture capital community has spoken with unequivocal clarity: the era of the generic AI SaaS startup is over. The staggering influx of capital into the artificial intelligence sector is now strictly reserved for entities that possess a true, enduring structural advantage. Simply utilizing a third-party LLM to perform basic task automation is no longer a viable business strategy; it is merely a feature that will inevitably be commoditized by the foundation model providers themselves.

To build a fundable, highly profitable, and sustainable enterprise in 2026, technology executives, CFOs, and founders must aggressively pivot from a mindset of basic experimentation to one of deep, architectural defensibility. This vital transition requires:

- Moving decisively away from fragile, low-cost "wrappers" and investing in high-value Systems of Action that autonomously execute complex, mission-critical workflows.

- Actively cultivating proprietary data flywheels where continuous user interaction refines the intelligence of the system, creating a compounding advantage.

- Rejecting the limitations of off-the-shelf compromises in favor of custom software engineering that guarantees intellectual property ownership, robust security, and seamless integration into legacy enterprise architectures.

- Dominating market distribution by embracing transparent, highly educational marketing frameworks like "They Ask, You Answer" to build unshakeable brand trust and a loyal customer base.

The artificial intelligence revolution is not inherently destroying the software industry; rather, it is forcing the software industry to rapidly evolve. The organizations that survive this critical inflection point will be those that view AI not as a cheap shortcut to market, but as a foundational, deeply engineered component of a highly specialized, defensible business model.

Frequently Asked Questions

Why are venture capitalists refusing to fund generic AI "wrappers"? Venture capitalists view thin wrappers—applications that simply put a user interface over an existing model like ChatGPT or Claude—as structurally fragile and ultimately unfundable. These startups lack unique intellectual property, have near-zero barriers to entry (leading to intense, margin-destroying competition), and face the constant, existential threat of being rendered obsolete overnight when the underlying model provider releases a similar feature natively.

What is the difference between an AI "Supernova" and a "Shooting Star"? According to comprehensive benchmarks established by Bessemer Venture Partners, "Supernovas" are AI startups that scale explosively (e.g., reaching $100M ARR in just 1.5 years) but often sacrifice gross margins and customer retention to achieve that breakneck speed. "Shooting Stars" follow a more traditional, sustainable SaaS growth trajectory (reaching $100M ARR in roughly 4 years) but maintain highly efficient capital metrics, exceptionally loyal enterprise customers, and strong gross margins of around 60%.

How can a B2B AI company build a defensible data moat? A true data moat is built by moving far beyond publicly scraped data to capture unique, proprietary information generated directly through user interactions. By creating a closed-loop "data flywheel," every edge case handled, correction made, or workflow completed by the user feeds directly back into the system, fine-tuning the proprietary model. This dynamic process makes the product continuously smarter, increasingly embedded in the client's operations, and exceptionally hard for competitors to replicate.

Why is custom software development recommended over off-the-shelf AI tools for enterprise defensibility? While off-the-shelf AI provides the allure of quick implementation, it offers absolutely no competitive differentiation and frequently struggles with complex, industry-specific workflows and strict security compliance. Custom software engineering ensures the business completely owns the intellectual property, seamlessly integrates the AI into its existing, proprietary databases, and tailors the system precisely to unique operational needs, thereby establishing a long-term, highly defensible strategic advantage.

How does the "They Ask, You Answer" approach help B2B software companies build a distribution moat? "They Ask, You Answer" is a strategic marketing framework centered on radical transparency and customer education. By proactively publishing detailed content that addresses a buyer's most pressing concerns—such as specific costs, potential implementation problems, and direct competitor comparisons—companies build massive trust and establish organic search dominance. This creates a powerful distribution and brand moat that significantly accelerates the enterprise sales process and protects against newly launched clones.

Where does human oversight fit into all this automation? Even the most advanced Systems of Action still need clear guardrails. Many enterprises are now adopting a 90/10 human-in-the-loop trust architecture, where AI handles 90% of the work but humans review the riskiest 10%. This balance keeps velocity high while protecting brand, compliance, and long-term enterprise value.

Supporting Industry Resources

- https://www.bvp.com/atlas/the-state-of-ai-2025

- https://techcrunch.com/2026/03/01/investors-spill-what-they-arent-looking-for-anymore-in-ai-saas-companies/

- https://www.impactplus.com/blog/they-ask-you-answer-b2b-examples

About Baytech

At Baytech Consulting, we specialize in guiding businesses through this process, helping you build scalable, efficient, and high-performing software that evolves with your needs. Our MVP first approach helps our clients minimize upfront costs and maximize ROI. Ready to take the next step in your software development journey? Contact us today to learn how we can help you achieve your goals with a phased development approach.

About the Author

Bryan Reynolds is an accomplished technology executive with more than 25 years of experience leading innovation in the software industry. As the CEO and founder of Baytech Consulting, he has built a reputation for delivering custom software solutions that help businesses streamline operations, enhance customer experiences, and drive growth.

Bryan’s expertise spans custom software development, cloud infrastructure, artificial intelligence, and strategic business consulting, making him a trusted advisor and thought leader across a wide range of industries.